2025 highlights

At a glance

Market position#2 2024: #2 | Customer base(in million)5.2 2024: 4.5 | Employees(in FTE)8,689 2024: 7,373 |

Carbon footprint reduction(in %)8.6 2024: 5.3 | Impact investments(in % of total AuM)10.1 2024: 8.7 | Employee engagement(in percentile)771 2024: 73 |

Sustainable reputation(in %)41 2024: 39 | Gender diversity(female as % of total management)34 2024: 32 | NPS-i(-100 to 100)25.0 2024: 18.42 |

| 1 Based on the most recent pulse check assessment from January 2026. The annual extensive culture scan, conducted in February 2025 had 71 as a result. 2 Please note the 2024 figure represents the Q4 baseline value. |

Dividend per share | Market capitalisation(in € billion)12.7 2024: 9.7 | Total assets(in € billion)142.2 2024: 138.6 | Total equity(in € million)10,124 2024: 9,8881 |

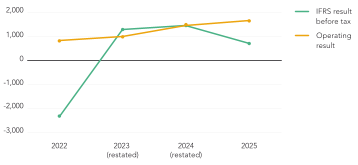

Operating result(in € million)1,637 2024: 1,4631 | IFRS net result(in € million)565 2024: 9561 | Operating return on equity(in %)14.1 2024: 13.41 | |

Solvency II ratio2 | Organic capital creation(in € million)1,315 2024: 1,193 | ||

Credit rating(S&P, IFSR)A+ 2024: A | 1 This figure is restated. 2 The Group Solvency II ratio is based on the Partial Internal Model (PIM), applicable to Aegon Life, Aegon Spaarkas and a.s.r. Life. The other insurance entities calculate their solvency capital requirement using the Solvency II Standard Formula. The Group Solvency II ratio includes financial institutions. |

Integration Aegon Nederland N.V.

This section describes the progress that has been made in the integration of Aegon Nederland N.V. (Aegon NL) with ASR Nederland N.V. (a.s.r.). Following the closing of the transaction in July 2023, a.s.r. committed to completing the integration within three years, by mid 2026. Since then, numerous milestones have been completed and the integration is well on track.

a.s.r. is now positioned to leverage the unique strengths of both organisations in support of a.s.r.'s strategic goal of creating a leading insurer in the Netherlands, enhancing the company's ability to deliver value across non-life and life insurance, pensions, asset management activities and distribution services. With the integration approaching it's final phase, the commercial and financial performance so far confirm the strategic and financial benefits of the combination with Aegon NL. a.s.r. remains committed to executing the planned integration path and delivering on its objectives.

Since the closing of the transaction in July 2023, a.s.r. has expeditiously executed the integration plan for Aegon NL, successfully completing nearly all key milestones. Policy migrations across P&C, Disability, Mortgages, Individual life and Pension have been finalised, marking a significant achievement in the integration journey by transferring over two million active policies spread over the different business domains. The programme has now entered its final phase and remains firmly on track for full completion by mid-2026, as originally planned. The remaining activities are focused on decommissioning the IT infrastructure and phasing out residual dependencies on Aegon Group systems. This year's update will therefore mark the final dedicated integration update.

With this transition, a.s.r. is not only delivering on its integration promise but also reinforcing its position as a leading insurer in the Netherlands. The combination of two strong organisations has already translated into tangible commercial and financial benefits, enabling a.s.r. to create more value across non-life and life insurance, pensions, asset management, and distribution services.

Further progress towards key milestones

In 2025, a.s.r. achieved several important integration milestones. On 1 January 2025, the legal merger of the IORP pension entities - Aegon Cappital B.V. and ASR Premiepensioeninstelling N.V. - was completed. The full integration of asset management activities followed shortly thereafter, with all associated Transitional Service Agreements (TSAs) terminated. By year-end, all non-IT TSAs had been phased out. Final systems decommissioning is scheduled for June 2026.

Earlier, in 2024, a.s.r. completed the migration of all Property & Casualty and Disability insurance policies from Aegon NL into its core systems - covering more than one million policies - making non-life the first major business line fully integrated. This milestone brought unified policy administration and processes under one platform, significantly enhancing operational efficiency.

The divestment of Knab was finalised on 1 November 2024. Knab now operates independently, with no remaining TSAs and only minor trademark-related arrangements. In the Mortgages domain, the migration process was fully completed in 2025. New mortgage production transitioned to the Stater platform early in the year, and by October, approximately 300,000 active mortgage accounts had been successfully migrated. In parallel, the Individual life portfolio migration was executed in phases, with the final portfolio migrated in Q4 2025. In total, around 550,000 life insurance policies were consolidated onto a.s.r.’s LeanApps platform, enabling the shutdown of Aegon’s separate life-policy systems and streamlining operations under a single administration.

A major milestone was achieved in December 2025, when the Dutch Central Bank (De Nederlandsche Bank - DNB) approved the Partial Internal Model for ASR Levensverzekering N.V.

Successful integration through simplicity and discipline: thorough preparation, strong collaboration and monitoring of results, all while keeping the business running.

Manager Corporate Development

Final steps towards full integration

The final phase of integration in 2026 will focus on completing the remaining steps and consolidating the one-company operating model. Key milestones include the legal merger of the life entities (planned for mid-2026) and the full decommissioning of Aegon NL systems and IT services. By mid-2026, all ITSAs between a.s.r. and Aegon Ltd. will be terminated, enabling the combined business to operate entirely on a.s.r.’s IT infrastructure. The Leeuwarden office is scheduled to be vacated by year-end 2026, once teams are fully operational at the Utrecht location.

Further optimisation of the Pension business line will continue beyond 2026, with a longer-term horizon (2027–2028) to harmonise Defined Benefit (DB) administration platforms and transition all DC administration to the target platform Plexus.

Achieving full run-rate cost synergies remains a top priority. a.s.r. expects to realise the remaining synergy benefits primarily through the elimination of IT transitional services and rationalisation of supporting teams. By mid-2026, the total projected synergies from the integration are expected to be fully captured, in line with the financial objectives set at the time of acquisition.

Governance to completion

Throughout the final stretch of the integration, a.s.r. has maintained strong governance and oversight. The last user migrations have been successfully finalised, and the decommissioning of legacy IT systems is progressing on schedule.

a.s.r. continues to support employees affected by the integration, balancing the additional workload with business-as-usual operations and facilitating transitions to new roles within or outside the company. These risks have been effectively managed through detailed planning and proactive mitigation measures. Senior management engagement remains high, and the Integration Management Office and steering committees will continue to monitor progress until all milestones are completed.

By the end of 2026, with all planned legal entity mergers, migrations and system decommissions finalised, the integration programme will be completed. The combined company will then transition to business-as-usual operations, operating with a unified culture, a single set of systems and fully materialised synergies. The valuable integration capabilities and lessons learned will be leveraged to ensure the efficient integration of future acquisitions.

1 Message

from the

CEO

Message from the CEO

Full circle

Dear reader, before you lies a.s.r.’s Annual Report for 2025. It was, once again, an exceptional year in the long history of a.s.r. It was the year in which we completed the integration of Aegon Nederland’s business units into our organisation. Following the joint announcement in October 2022 of our intention to merge, we successfully achieved this objective within the targeted 2.5 years. By the end of 2025, all major migrations had been completed, resulting in one organisation with one way of working for all customers. This marks one of the largest integrations in the Dutch insurance market, and I am proud of everyone who has contributed to this milestone.

As the integration progressed, our business continued to deliver strong results. We strengthened a.s.r. through several important transactions, including the real estate transaction involving Amvest and the acquisition of the funeral insurance portfolio of the oldest insurer in the Netherlands. We also expanded our position in occupational health services and reintegration by becoming the 100% shareholder of HumanTotalCare. Early in 2026, we announced the intended acquisition of the insurance activities of Bovemij, further reinforcing our position in the Non-life market.

In 2025 we completed several pension buy-outs, ensuring pension security for many participants. We also concluded the long-running unit-linked file. More than 90% of affiliated customers accepted the agreement reached with interest groups. This brought collective proceedings to an end, with the groups agreeing not to initiate new proceedings. It closed a complex and impactful file constructively for all stakeholders.

These developments all contribute to our objective of creating long-term value creation for our stakeholders.

Our financial and non-financial results over 2025 are strong and meet or exceed our targets. The significant increase in customer appreciation is a welcome recognition of the dedication of our employees, to whom I am sincerely grateful. Employee satisfaction, measured again in January 2026, shows an upward trend - an outcome that reflects, among other things, the successful execution of the integration.

Every day, we work towards building a more sustainable world. We continued reducing the CO₂ footprint of our investment portfolio and increasing our impact investments. Our CO₂ footprint decreased by 8.6% in 2025, keeping us on track to achieve our 2030 target of 25%. Impact investments reached 10.1% of total investments, enabling us to meet our 2027 target of 10% ahead of schedule.

Our financial results underline a.s.r.’s strong position in the Dutch market. Premiums and DC inflow increased by 28.9%, and the operating result rose by 11.9%. Our capital position remains robust, with organic capital creation up by 10.2%. With the approval of the Partial Internal Model (PIM) for ASR Levensverzekering N.V., we now report under Solvency II based on the PIM for all Life entities. This contributed to the Solvency II ratio increasing to 218%. In 2025, we repurchased € 230 million of our own shares, and upon publishing our annual figures on 18 February 2026, we announced an additional repurchase of € 175 million - fully in line with our strategy to deploy capital to create value and efficiently return capital to shareholders.

As a Dutch insurer, we understand the local market well. At the same time, we remain mindful of shifting geopolitical dynamics that influence decisions related to investments, risk and long-term security. We take responsibility for societal themes where we can genuinely make an impact - such as the housing shortage, climate risks, sustainable employability and income security. We follow developments from the new government closely and are ready to contribute our insights to help build a better Netherlands for today and for future generations.

This is the eighteenth Annual Report of a.s.r. in its current form, and once again I have the privilege of addressing you as CEO and Chair of the Executive Board. Since 2008, a.s.r. has undergone several transitions. In our 2008 Annual Report, I wrote: 'In retrospect, 2008 has been a harsh learning experience for the financial sector. We cannot change the past, but we can change our future.' That was our impetus to return to the core of our company: insuring risks that people are unable or unwilling to bear themselves, and building capital for the future. Our guiding principle has been the Rijnlands model, ensuring that we consider the interests of all stakeholders. With that compass, I have dedicated myself to a.s.r. since then.

I began my career at Stad Rotterdam, then a listed and prominent insurer and one of the legal predecessors of a.s.r., with roots dating back to 1720. Through its incorporation into Fortis, the nationalisation in 2008, and our successful return to the private market through the IPO in 2016, we have built a strong team and a healthy, solid organisation. With a clear growth-oriented strategy, well positioned for the future. This is not the achievement of executives alone. Strategies and plans may set the direction, but real progress is driven by the commitment of colleagues who have contributed over the years. I would therefore like to express my sincere appreciation to all our employees for their dedication. I also thank our shareholders and customers for the trust and confidence they continue to show.

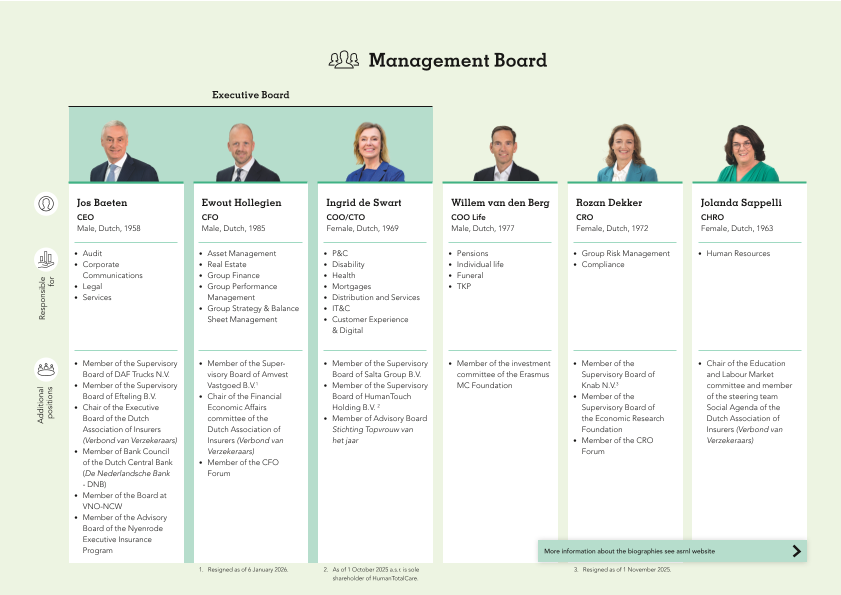

After more than 45 years at a.s.r. and its predecessors, the circle is complete for me. This 2025 report is my last Annual Report as CEO and I recognise that a long and rewarding period at a.s.r. is coming to an end. I am pleased that the Supervisory Board has nominated Ingrid as my successor. She has been a member of the Executive Board for 6.5 years, and during that time I – together with my colleagues in the MB - have worked with her with great pleasure and in a highly constructive manner. She is among the best executives in the Dutch insurance sector. Knowing that a.s.r. will be in excellent hands with her, I pass on the baton with full confidence. I wish her, and all colleagues at a.s.r., every success for the future.

Jos Baeten

CEO and chair of the Executive Board

2 Business and strategy

2.1 The story of a.s.r.

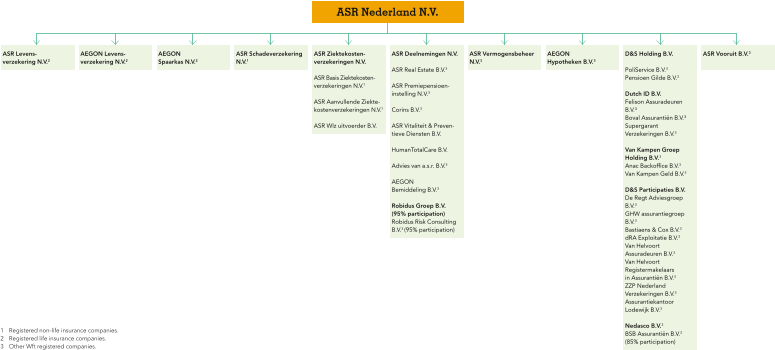

ASR Nederland N.V. (a.s.r.) is the second-largest insurer in the Netherlands and is listed on Euronext Amsterdam, where it is included in the AEX Index. a.s.r. offers services and products in the field of insurance, pension and mortgages, and acts as an asset manager for third parties.

Mission

The mission of a.s.r. is to help customers insure risks they are unwilling or unable to bear themselves, and to accumulate capital for later. It's products and services are designed for the long term, with future generations in mind, serving private individuals, self-employed professionals and businesses - now, later and always.

a.s.r. aims for sustainable growth, guided by the principle of value over volume. It does so by helping its customers strengthen their financial security, by expanding its role in society, and by investing in innovation that truly makes a difference.

Strategy

a.s.r. aims to create long‑term value for its key stakeholders: customers, employees, shareholders and society. It strives to be the leading pension provider in the Netherlands and a leading mortgage lender. Its ambition is to strengthen its position and pursue growth in Property and Casualty (P&C), Disability and Asset Management in the coming years, while maintaining its current position in Health and Individual life & Funeral. a.s.r. also seeks to expand its role in the value chain through distribution and service companies.

To become the best in the industry, a.s.r. embraces technological developments and applies them where they add value. a.s.r. operates cost‑efficiently and is financially robust, managing the funds entrusted to it by customers with care. Financial strength is essential to meet obligations and provide continuity for customers and employees. Shareholders are offered the prospect of a fair return.

Customers

a.s.r. strives to be the best financial service provider for its customers and intermediaries. It offers simple and transparent products and services that meet customers’ needs, including sustainable solutions. Customers can rely on a.s.r. to meet its obligations.

a.s.r. aims for customers and advisers to rate its products and services above average. To achieve this, a.s.r. works closely with intermediaries who understand customers’ personal situations and can provide tailored advice. Customers also have the flexibility to manage matters quickly and easily through the digital environment, or opt for personal contact when needed. a.s.r. is data‑driven and incorporates customer feedback into its decision‑making. By leveraging technological innovations, including Artificial Intelligence (AI), a.s.r. continuously improves its services.

Employees

Talented, skilled and vital employees are key to a.s.r.’s success. Every day, employees are committed to supporting customers and advisers in the best possible way. Everyone at a.s.r. works according to three core values to achieve this goal:

We are helpful – Acting with the customer and adviser in mind, understanding their needs, aligning carefully and honouring commitments.

We think ahead – Preparing thoroughly, listening attentively and providing appropriate solutions based on expertise, experience and dedication.

We achieve results – Focusing on content and process, taking responsibility and completing what has been started. In doing so, the desired outcome is achieved together.

a.s.r. aims to ensure that employees remain healthy and sustainably employable. With trust as its foundation, a.s.r. seeks to foster an inclusive culture and a supportive working environment with a strong customer focus.

Employees are expected to demonstrate courage and personal leadership. To support this, a.s.r. empowers employees to take ownership of their careers by investing in personal development and by offering opportunities to expand relevant knowledge and skills. In addition, a.s.r. actively promotes physical and mental health and encourages social engagement to help maintain a healthy work–life balance.

Shareholders

a.s.r.’s focus on long‑term value creation and pursuit of profitable growth, progressive dividends and additional capital returns supports shareholder value. Shareholders can rely on a.s.r. being financially robust and manage the capital entrusted to us responsibly. They may expect solid financial performance, a strong balance sheet, economically rational capital allocation, disciplined cost management and transparent reporting.

Society

As a major insurer, a.s.r. seeks to contribute to solving societal challenges by focusing on the three pillars where it can make the most impact:

Financial self-reliance and inclusion

a.s.r. helps people take responsible risks and make conscious financial choices. The aim is to prevent people from falling into debt or support them in resolving debt. Particular attention is given to the inclusion of diverse target groups, including vulnerable groups within society.

Vitality and sustainable employability

a.s.r. is committed to preventing illness, absenteeism and incapacity for work among employees, employers and healthcare customers. This approach enables people to work longer and healthier and continue to contribute to society.

Sustainable living and climate

To reduce its ecological footprint, as a major (real estate) investor, a.s.r. invests in activities that mitigate climate risks, support the energy transition and restore biodiversity. Customers are supported with insurance products and advice on how to live more sustainably. Within its own operations, a.s.r. makes conscious choices to minimise the environmental impact of offices, transport and procurement. And by making smart decisions and sustainable investment choices, its social impact develops alongside organisational growth.

Society can expect a.s.r. to integrate environmental, social and governance objectives into its strategy.

2.2 Business portfolio and group value chain

2.2.1 Business portfolio

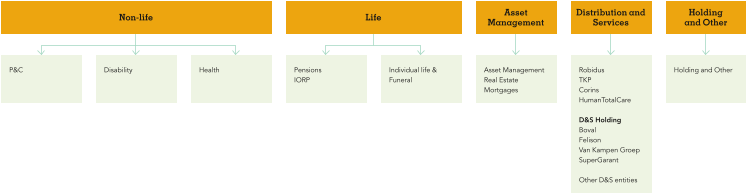

a.s.r.'s business portfolio consists of five segments, as illustrated in the figure below. For more information about these segments, see section 4.

Non-life

The Non-life segment consists of the non-life insurance entities and their subsidiaries. These entities offer non-life insurance contracts such as P&C, disability and health.

P&C

a.s.r. ranks among the top three P&C insurers in the Netherlands, with a market share of 14.7% (2024: 14.7%) measured by GWP.1 a.s.r. offers the following P&C products:

Motor insurance;

Fire insurance;

Other insurance products, such as liability, legal aid, travel and recreation, pet and transport insurance.

These products are offered to both retail and commercial customers under the a.s.r. brand and the label Ik kies zelf van a.s.r. The a.s.r. brand serves retail and commercial markets primarily through independent advisors and mandated brokers. The Ik kies zelf van a.s.r. label focuses on direct online distribution to individuals and offers travel and leisure insurance via travel agents.

Disability

a.s.r. is the leading insurer in the disability market, offering income protection. It has an extensive range of products and services focusing on sustainable employability and on preventing and reducing absenteeism. Distribution of disability insurance products takes place mainly through insurance advisors. With the brands a.s.r. and Loyalis, a.s.r. is well positioned in this distribution channel, serving self-employed individuals, SMEs, corporates and the (semi-) public sector. a.s.r. is the market leader, with a market share of 39.5% (2024: 39.8)%1.Through its prevention and reintegration services, a.s.r. helps its customers to ensure optimal employability for themselves and their employees.

a.s.r.’s income protection insurance business offers various products divided into the following product groups:

Individual disability;

Sickness leave;

Group disability.

Health

a.s.r. offers basic health (medical) insurance under the Dutch Health Insurance Act (Nederlandse Zorgverzekeringswet) in combination with supplementary health insurance. It does so under the brand a.s.r. and under the label Ik kies zelf van a.s.r. With around 700,000 customers, a.s.r. is the seventh largest provider of health insurance on the Dutch market with a market share of 2.4% (2024: 3.2%).1

Life

The Life segment consists of Pensions, Individual life & Funeral. The Life segment has a market share of 24.2% (2024: 28.6%).1

Pensions

a.s.r. is a major provider of Defined Contribution (DC) pensions in the Netherlands. It provides different propositions for premium build-up with lifecycle solutions for SMEs and large-cap companies:

The Employee pension (Werknemerspensioen) (a.s.r. Life);

Doenpensioen van a.s.r. (a.s.r. IORP);

Cappital Pensioen (a.s.r. IORP).

Individual life & Funeral

Individual term life insurance is the only individual life product that a.s.r. actively sells. It guarantees payment of a death benefit to the insured's beneficiaries if the insured dies during the specified term.

a.s.r. is a top-three funeral insurer in the Netherlands, selling funeral capital insurance policies that enable customers to fund their own funeral.

Asset Management

The Asset Management segment involves all activities relating to asset management, including investment property management.

Asset Management

a.s.r. asset management (a.s.r. vermogensbeheer) manages assets for a.s.r.'s own account and offers asset management services for affiliated entities as well as third parties. The investment categories include primarily corporate bonds, government bonds and equity. This way, a.s.r. asset management offers investment solutions with attractive returns.

Real Estate

a.s.r. real estate invests in real estate and infrastructure (real assets) on behalf of a.s.r. and third-party institutional investors and manages real assets portfolios. a.s.r. owns a 50% interest in the joint venture Amvest Vastgoed B.V. And the joint venture Amvest Development Fund B.V. On 8 July 2025, a.s.r. and the Dutch pension fund for the care and welfare sector (Pensioenfonds Zorg en Welzijn - PFZW), agreed to divide Amvest's real estate activities. This transaction was approved by the Dutch Authority for Consumers and Markets (Autoriteit Consument & Markt - ACM) and the Dutch Authority for the Financial Markets (Autoriteit Financiële Markten - AFM) in November 2025 and the closing was early January 2026.

a.s.r. real assets investment partners develops investment strategies, ensures their implementation and gives institutional investors control over real asset portfolios through active monitoring, reporting and engagement.

Mortgages

a.s.r. mortgages operates in the residential mortgage market. a.s.r. also offers third party investors the opportunity to invest in Dutch residential mortgages. a.s.r. has a market share of approximately 7%.

a.s.r. mortgages offers its mortgage products to customers via intermediaries, under two different mortgage brands: a.s.r. and Aegon. Under the Aegon brand, standard products (annuity, linear and interest-only mortgages) are offered to a broad customer base. In addition to standard products, the a.s.r. brand offers specialised products for distinct customer groups. This includes products for first-time buyers, customers who want to finance sustainable home modifications and senior citizens.

Distribution and Services

The Distribution and Services (D&S) holding company is responsible for a.s.r.'s distribution and service entities. Companies under D&S are jointly responsible for developing a centralised strategy and promoting cooperation and synergy between the businesses. These companies retain their own unique identities and organisational structures. They continue to operate independently of a.s.r. but in line with the a.s.r. strategy.

Holding and Other

The Holding and Other segment (including eliminations) consists primarily of the following activities:

Holding activities of a.s.r., including group-related activities;

Other holding and intermediate holding companies, including:

ASR Real Estate Development B.V., the real estate development business;

ASR Vooruit B.V., the investment firm that performs activities relating to private investments for customers;

ASR Deelnemingen N.V.

- Market shares DNB 2024. Market shares 2025 are not available yet at time of publication of this report.

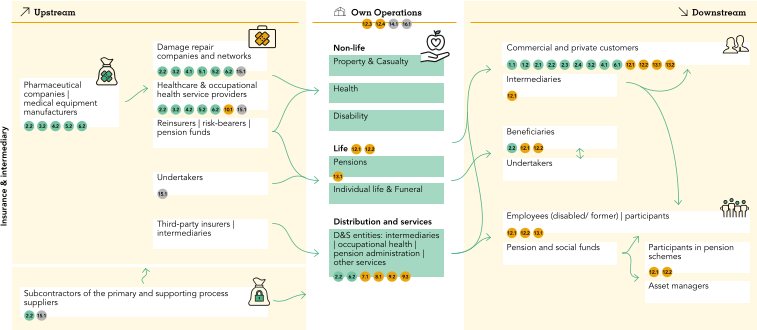

2.2.2 Group value chain

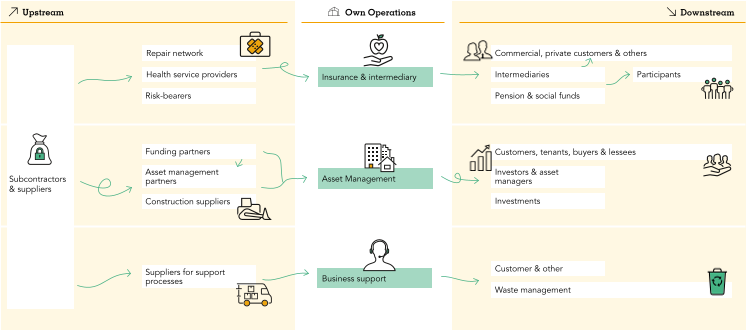

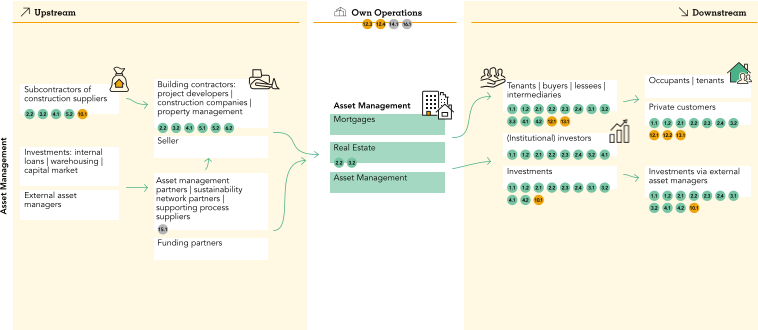

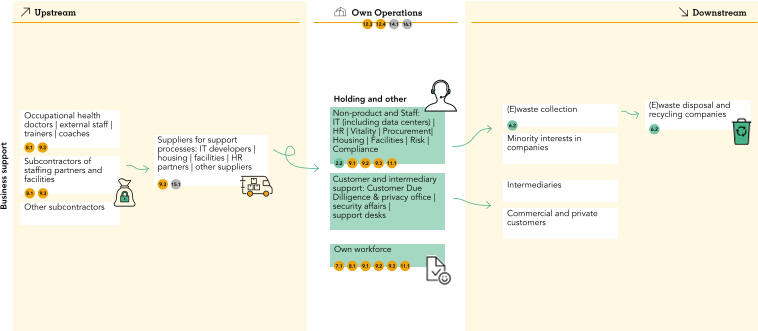

In accordance with the Corporate Sustainability Reporting Directive (CSRD), a.s.r. conducted a Double Materiality Assessment (DMA). This assessment is a crucial step in defining the organisation's reporting scope for its most material sustainability topics and in mapping its value chain. The value chain outlines a.s.r.'s business operations and its associated upstream and downstream business relationships.

Upstream value chain

The upstream part of the value chain comprises suppliers of goods and services, contractors and capital providers that are essential for the functioning of a.s.r.'s business activities.

Own operations

a.s.r.’s business activities cover a range of financial services, which are organised into five segments as outlined in the business portfolio (see section 2.2.1). These segments align with the group value chain according to their respective activities:

Insurance and intermediary: Combines three segments, Non-life, Life and Distribution and Services, based on their insurance-related activities.

Asset Management: Includes Mortgages, Real Estate and Asset Management.

Business support: Includes a.s.r.’s own workforce and the activities within the Holding and Other segment that provide staff and support functions. Certain activities within the Holding and Other segment, such as real estate developments, are presented under their respective business activities within the group value chain.

Downstream value chain

The downstream value chain includes a wide range of actors, such as consumers and end-users, intermediaries and waste management companies. a.s.r. offers non-life and life insurance products and services to both business and private customers via intermediaries, mandated brokers and direct online distribution.

a.s.r. is a multi-product organisation involving various internal and external stakeholders. The value chains of seperate product lines have been mapped and grouped into three overarching value chain segments based on the nature of their activities: Insurance and intermediary, Asset Management and Business support. Descriptions of these segments are provided in sections 2.2.1 and 6.1.4.4. The consolidated value chain, derived from these underlying value chains, is presented below.

- Section 2.2.2 is in scope of CSRD and limited assurance (ESRS 2 SBM-1)

2.3 How a.s.r. creates value

How a.s.r. creates value

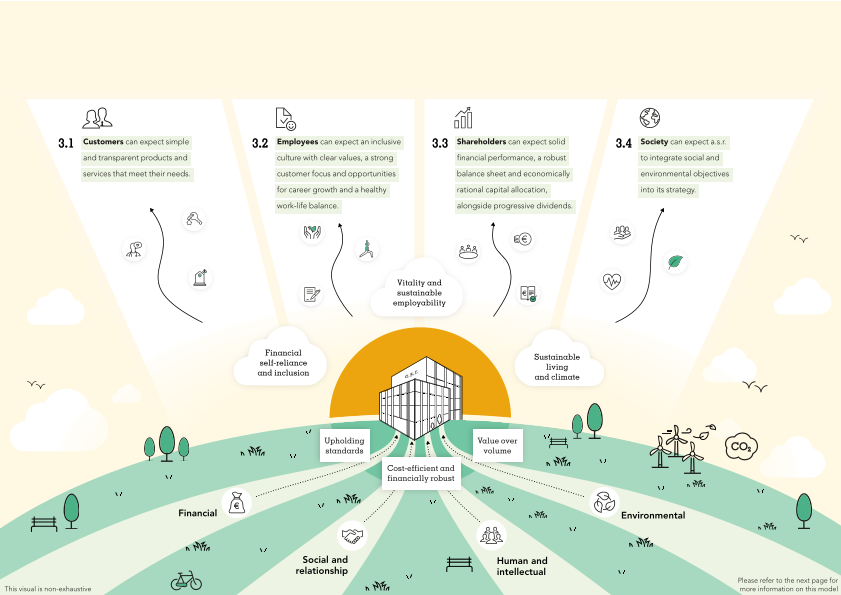

The mission of a.s.r. is to help customers insure risks they are unwilling or unable to bear themselves, and to accumulate capital for later. This value creation model illustrates how a.s.r. translates this mission into long‑term value for its stakeholders. It provides a clear overview of how a.s.r. transforms resources into responsible outcomes, reinforcing the organisation's purpose and responsibilities.

The model starts at the bottom, where the inputs represent the essential resources on which a.s.r. depends: financial, social and relationship, human and intellectual, and environmental capital.

Moving upward, the model highlights a.s.r.’s guiding principles: upholding standards, prioritising long‑term value over volume and maintaining cost efficiency to ensure financial health. These guiding principles form the foundation on which the organisation's activities are carried out and enable resources to be transformed into long‑term value for stakeholders.

Building on this foundation, a.s.r.’s strategic agenda includes three sustainability pillars: Financial self-reliance and inclusion, Vitality and sustainable employability and Sustainable living and climate. These pillars guide the company's efforts to create positive impact for society and the environment, while minimising its negative impact.

At the top, the model presents the expected outputs and outcomes, organised by stakeholder group. These illustrate the results of a.s.r.’s actions:

Customers can rely on a.s.r.’s transparent and responsible products and services, and dedication to long-term financial security. The customer base mainly consists of private individuals, self‑employed professionals and businesses. For more information, see section 3.1.

Employees experience an inclusive culture that values respect and recognition, while supporting personal development and customer focus. For more information, see section 3.2.

Shareholders benefit from a.s.r.’s commitment to value creation, cost discipline, transparent reporting, and economic rational capital allocation. For more information, see section 3.3.

Society can expect a.s.r. to integrate social, environmental and governance considerations into its strategic agenda, while ensuring that its activities align with regulatory requirements. For more information, see section 3.4.

a.s.r. puts value over volume in pursuit of long-term value creation for all stakeholders.

Director Investor Relations and Ratings

2.4 Strategic targets and material topics

a.s.r. aims to achieve sustainable and profitable growth by executing a disciplined strategy centred on organic growth and efficient capital allocation. It prioritises value over volume, maintains strict cost discipline and selectively pursues bolt-on acquisitions. a.s.r. is committed to delivering attractive returns, safeguarding a resilient balance sheet and operational excellence across all product lines. By maintaining strong financial flexibility and a robust Solvency II ratio, a.s.r. positions itself as a leading insurer in the Netherlands, ready to capture growth opportunities while ensuring long term value creation.

a.s.r. embeds sustainability at the heart of its strategy, focusing on three key pillars: Financial self-reliance and inclusion, Vitality and sustainable employability and Sustainable living and climate. Through these pillars, a.s.r. seeks to contribute to solving societal challenges and aims to reduce its environmental footprint and support the transition to a low-carbon economy, promote healthy and future-proof lifestyles for customers and employees, and strengthen financial resilience and inclusion across society. By combining financial strength with societal impact, a.s.r. strives to accelerate the transition towards a sustainable economy.

2.4.1 Strategic targets

a.s.r.’s strategy, presented at the 2024 Capital Markets Day (CMD), focuses on long‑term sustainable value creation for all stakeholders. It is built on value‑over‑volume, financial discipline and the rational allocation of capital. The strategy is driven by clear priorities that support growth, efficiency, capital flexibility and ESG leadership:

Drive sustainable and profitable growth across all business lines, including Non-life, Life and Fee based businesses.

Strengthen customer and intermediary relationships.

Improve efficiency and enhance income through operational excellence and investment performance.

Pursue selective M&A to add scale and capabilities.

Optimise capital and financial flexibility.

Maintain leadership in ESG.

Profitable growth and sustainable value creation is underpinned by:

Proven track record in disciplined execution of strategy, strong performance and consistent delivery on ambitious targets.

Demonstrated performance in rational capital allocation and delivering attractive returns.

In 2025, a.s.r. delivered strong results and made significant progress towards achieving its ambitious goals for the 2024–2026 period.

2.4.1.1 Financial targets

The combined business is leading in various market segments, and a.s.r. sees ample opportunities for profitable growth and to create sustainable value for all stakeholders. a.s.r. is well-positioned to benefit from the structural pension market developments and continues to pursue profitable growth in P&C and Disability, maintaining a strong combined ratio and underwriting performance. Furthermore, a.s.r. aims to supplement organic growth with strategic bolt-on acquisitions to add scale and skills. This is reflected in ambitious group and business targets.

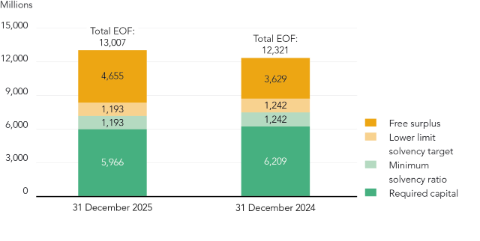

Solvency II ratio2

This metric is based on the Solvency II framework and represents the solvency position of a.s.r. The Solvency II ratio is an integral part of a.s.r.'s Solvency II management ladder. This ladder represents different levels of solvency that is required for paying dividends (>140%), being entrepreneurial (>160%) in terms of organic and inorganic growth and re-risking, and considering additional capital return to shareholders (>175%).

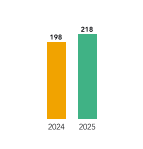

The Solvency II ratio increased to 218% (31 December 2024: 198%) with organic capital creation (OCC) (21%-points) offsetting the deployment of capital (-21%-points), including pension buy-outs, acquisitions and capital distributions. The positive impact of the implementation of the Partial internal model (PIM) for ASR Levensverzekering N.V. and related capital management actions is circa 12%-points on the group Solvency II ratio. Market and operational developments contributed positively (7%-points).

Organic capital creation

The OCC is an operating profit measure (after tax) within the Solvency II framework. The OCC reflects three key components: business capital generation, finance capital generation and net SCR impact.

The OCC increased by € 122 million to € 1,315 million (2024: € 1,193 million), primarily driven by higher finance capital generation, improved business performance and the realisation of cost synergies. The increased finance capital generation reflects a higher investment margin resulting from re-risking of the investment portfolio (mainly executed in second half of 2024), wider government bond spreads, positive equity and real estate revaluations and interest rate developments (e.g. a reduced UFR drag).

Operating return on equity3

Capital return4

Total capital return comprises dividends and share buybacks.

Dividend per share

a.s.r. strives to pay annual dividend that creates sustainable long-term value for its shareholders. From 2022 onwards, a.s.r.’s Dividend Policy offers a progressive dividend to shareholders. This dividend is determined discretionally and not tied directly to a single financial performance metric. Following the announcement of the Aegon NL transaction in 2022 a.s.r. announced that it intends to pay a progressive dividend that would grow ‘mid-to-high’ single digit annually until (and including) 2025. At the CMD on 27 June 2024 a.s.r. announced that the period will be extended until 2026.

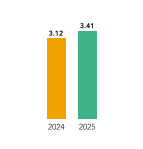

a.s.r. proposes a final dividend for 2025 of € 2.14 per share, bringing the total dividend (including interim dividend of € 1.27 per share) to € 3.41 per share, an 9.3% increase versus 2024 (€ 3.12 per share).

Share buyback

The projected developments of a.s.r.'s OCC in combination with a robust balance sheet enable the resumption of supplementary capital distribution to shareholders. Alongside a progressive dividend a.s.r. intends to provide an attractive capital return in the years ahead, a.s.r. also intends to allocate € 525 million to share buybacks over the plan period (€ 125 million over 2024, € 175 million over 2025 and € 225 million over 2026).

The € 330 million cumulative share buyback refers to the € 100 million share buyback following the completion of the sale of Knab, executed in 2024. The € 125 million announced share buyback with the 2024 annual results in February and € 105 million in September as participation in the sell-down of Aegon Ltd., executed in 2025.

The share buyback of € 175 million announced on 18 February, 2026 (in line with the medium-term targets as presented at the 2024 CMD) will be executed in the first half of 2026 and deducted from HY 2026 Solvency II ratio.

Non-life combined ratio and revenue growth

Combined ratio

Revenue growth

The combination of these targets reflect a.s.r.'s aim for profitable growth in P&C and Disability, pairing a strong combined ratio with premium growth.

The organic growth in P&C and Disability amounted to 3.0%, within the 3-5% target range. Growth in P&C and Disability mainly reflects price increases to mitigate claims inflation.

Pensions and Annuities

Total inflow in Pensions includes € 2,810 million AuM in pension buy-outs, € 3,011 million DC inflow (+8.8% vs 2024) and € 646 million annuities inflow (+11.2% vs 2024).

Pension buy-outs

a.s.r. aims to acquire € 8 billion of assets under management related from corporate pension funds in the period 2024 – 2027. Pension buy-outs amounted to € 2.9 billion Assets under Management (AuM) in 2025.

Pension DC inflow

Pension DC inflow increased to € 3.0 billion (2024: € 2.8 billion) driven by organic growth. The annuity inflow increased to € 646 million (2024: € 581 million), reflecting higher DC accumulation and increased maturity of DC AuM.

Annuities

As part of the Life segment, a.s.r. expects to benefit from the pension reform in the Netherlands and grow in DC pensions and annuities. Growth in the pension DC business is measured by inflow of DC products, where a.s.r. targets € 8 billion of DC inflow cumulatively in the plan period 2024 – 2026. For annuities a.s.r. targets € 1.8 billion of inflow cumulatively in the plan period 2024 – 2026.

Fee-based business operating result

The operating result of the fee-based businesses comprises of the result from segment Asset Management and segment Distribution & Services.

Fee-based business operating result

The operating result of the fee-based businesses increased by € 36 million to € 186 million (2024: € 150 million).

Cost synergies

At the announcement of the Aegon NL transaction on 27 October 2022, an overall run-rate cost synergy target of € 185 million for the combined companies was announced. This was raised one year later at an Investor Update on 30 November 2023 to € 215 million, after further detailing the integration plan. a.s.r. is on track to achieve this € 215 run-rate cost synergies in 2026.

- Targets are based on the assumption of normal (financial) markets, environmental and economic conditions and no material regulatory changes.

- The Group Solvency II ratio is based on the Partial Internal Model (PIM), applicable to Aegon Life, Aegon Spaarkas and a.s.r. Life. The other insurance entities calculate their solvency capital requirement using the Solvency II Standard Formula. The Group Solvency II ratio includes financial institutions.

- The operating return on equity is calculated by dividing the (annualised) operating result after deduction of taxes (taking into account the structural tax exempt dividend results) by the annual average equity attributable to shareholders after deduction of the reserve for unrealised profits and losses and the equity for Knab (operating activities in ‘run-off’).

- In general, a.s.r. expects not to pay cash dividends if the SII ratio falls below 140%. For SBB, the Solvency II ratio needs to be at least 175% with sufficient OCC to fund capital distributions and no alternative deployment of capital delivering superior returns, and to be decided annually upon discretion by the Management Board.

2.4.1.2 Non-financial targets

This section presents the non‑financial targets introduced during the CMD 2024.1

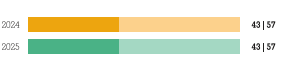

Net Promoter Score-interaction

In 2025, for the first time, a.s.r. is reporting on its Net Promoter Score for customer interaction (NPS-i), a customer satisfaction metric based on both online and offline channels. NPS-i represents the weighted average score of the NPS-c (Net Promoter Score for contact moments between client and a.s.r.) and NPS-d (Net Promoter Score for digital client interaction, e.g. website or online portal). Closely monitored through NPS surveys, the NPS-i, gives insight into the customer experience and highlights areas for improvement. These surveys have provided valuable feedback during the integration and migration of Aegon NL customers to a.s.r. products. The target for NPS-i is +4 at year-end 2026, compared to the Q4 2024 baseline of 18.4.

NPS-i2

In 2025, a.s.r. made further progress in strengthening customer centricity and improving the customer experience across online and offline channels. The NPS‑c remained consistently high during 2025 and the NPS-d continued to improve in 2025 resulting in a yearly average of 25.0 for the NPS-i (Q4 2025: 27.3) More information about NPS-i, see section 3.1.1.1

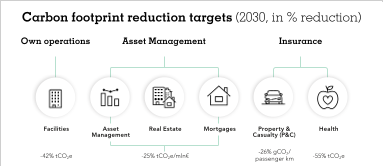

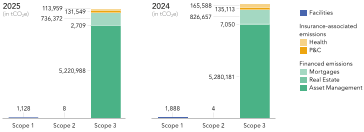

Carbon footprint reduction

Climate change is a material topic for a.s.r. Through its asset management activities, a.s.r. potentially makes a difference by engaging with investees to reduce their carbon footprint. On the CMD in June 2024, a.s.r. announced its target to reduce the carbon footprint of its internally managed own account assets and 3rd party assets by 25% in 2030, compared to base year 2023. This target builds on the carbon footprint reduction of 69% achieved between 2015 and 2023. Calculation of emissions is in line with the GHG Protocol scope 3 category 15: investments and the PCAF methodology for financed emissions. For more information about the methodology and score, see section 6.2.1.6.

Carbon footprint reduction

The carbon footprint of the investment portfolio decreased by 8.6% at 31 December 2025 compared to base year 2023, remaining on track to meet the 2030 target of -25%. The reduction is driven by lower emissions across various asset classes, particularly in mortgages and real estate. For more information about a.s.r. climate ambitions, see section 6.2.1.6

Impact investing

a.s.r. aims to generate positive impact through its impact investments while also generating attractive investment returns. The impact investment target is 10% of own account assets and internally managed affiliated assets by 2027. In line with the Global Impact Investing Network (GIIN), a.s.r. defines an investment as impact investment when it seeks to generate positive, measurable social and environmental impact alongside financial return. For more information about the specific criteria that apply and the scope of impact investing, see section 3.1.3.4.

Impact investing

Impact investments accounted for 10.1% of the investment portfolio as at 31 December 2025, a 1.4%-points increase compared to 31 December 2024 (8.7%). This increase mainly relates to an increased allocation in labelled bonds and social impact investments. As a result, the target for 2027 has already been achieved. For more details on impact investing in the business lines Asset Management, Real Estate and Mortgages, see section 3.1.3.4.

Employee engagement

a.s.r. strives to be an attractive employer. Engaged employees are key for a.s.r. to successfully execute its strategy. a.s.r. measures employee engagement via the annual Denison scan. Four themes are central: vision, core values and behaviour, empowerment and knowledge development. The key performance indicator (KPI) is expressed as a percentile and compared against a large, global benchmark. The target covers all a.s.r. employees including contractors, temporary workers and seconded workers with an a.s.r. contract and interns. Employees of subsidiaries are not in scope of this target. For more information regarding this target, see section 6.3.1.4.

The 2024 score serves as a baseline measurement, as it was the first year in which the KPI was tracked for the combined company. For the 2024–2026 target period, a growth trajectory has been defined. The target for 2025 is set at a minimum of 80, and for 2026 at a minimum of 85.

Employee engagement3

During 2025, employee engagement further decreased to the 71st percentile, reflecting the effects of the integration with Aegon NL, which was completed this year. Significant differences in scores can be observed between business units. Business units where the integration has already been completed score considerably higher than those where the integration has only recently begun or has yet to start. A more recent shortened survey conducted in January 2026 measured an increase to the 77th percentile, indicating a shift in sentiment.

Sustainable reputation

a.s.r.’s sustainable reputation score is crucial for its corporate strategy and market positioning. The survey, conducted by an independent expert organisation, measures the score on the following attributes: honesty, sustainability, reliability, and social responsibility. This KPI shows a.s.r.'s score based on surveys under Dutch people aged 18 to 65 years, with respondents giving a score per attribute of between 0% and 100%. The target is to achieve a score of 38-43% in the period 2024-2026.

Sustainable reputation

The sustainable reputation score rose to 41% in 2025 (2024: 39%), remaining within the target range of 38–43%. The increase is supported by campaigns that focus on sustainable damage repair and the collaboration with the Royal Dutch Walking Association (Koninklijke Wandelbond Nederland - KWbN). These campaigns contributed to the strategic pillars Sustainable living and climate and Vitality and sustainable employability.

Gender diversity

a.s.r. strives for a workforce that reflects society. Studies show that diversity in the workforce provides broader perspectives and enriches decision-making. The diversity target applies to employees in management positions and aims for at least 40% women and at least 40% men within the Supervisory Board (SB), Management Board (MB) and management by 2026. Management includes senior, higher and team management. For more information on gender diversity in a.s.r.'s workforce, see section 6.3.1.

Supervisory Board

Management Board

Management

On Supervisory Board (SB) and Management Board (MB) level, the gender diversity remains unchanged. On management level, gender diversity improved slightly towards the target level of at least 40% at end of 2026. In 2025, initiatives were taken to further improve gender balance such as an adjusted hiring procedure and additional part-time options.

- a.s.r. explanatory notes to Alternative Performance Measure - Non-financial targets 2024-2026.

- Please note the 2024 figure represents the Q4 baseline value.

- Based on the most recent pulse check assessment from January 2026. The annual extensive culture scan, conducted in February 2025 had 71 as a result.

2.4.2 Material sustainability topics and connectivity

Introduction

As previously outlined, a.s.r.’s strategic agenda includes the three sustainability pillars where a.s.r. can make the greatest impact: Financial self-reliance and inclusion, Vitality and sustainable employability and Sustainable living and climate.

A key element of a.s.r.’s sustainability strategy is to identify the topics where the organisation has the greatest impact and which are most relevant to its business and stakeholders. To achieve this, a.s.r. regularly conducts a Double Materiality Assessment (DMA). This assessment considers both perspectives: the potential impact of a.s.r. on people and the environment (the ‘inside-out’ view) and the risks and opportunities that sustainability topics may present for a.s.r. itself (the ‘outside-in’ view).

By applying this double perspective, a.s.r. obtains a comprehensive picture of the sustainability issues most material to its long-term strategy. The 2025 update of the assessment resulted in ten material sustainability topics that represent a.s.r.’s most important impacts, risks and opportunities. For more details on the assessment and its outcomes, see sections 6.1.4.2. and 6.1.4.3.

To advance its strategy, a.s.r. has set specific targets to ensure strategic alignment and maintain focus. This balanced approach combines both financial and non-financial objectives. For more information, see section 2.4.1.

a.s.r. aims to contribute to a number of the the United Nations Sustainable Development Goals (SDGs) where they are connected with its strategic pillars. For more information on how a.s.r. contributes, see section 8.3.

Connectivity matrix

The elements of a.s.r.'s strategy are closely interconnected, with the three strategic pillars guiding actions to create long-term value for customers and intermediaries, employees, shareholders, and society. This integrated approach enables a.s.r. to address its most material impacts, risks and opportunities, while driving progress on strategic targets. The table on the next page illustrates the connectivity within a.s.r.'s strategy between the strategic pillars, the key stakeholders served by a.s.r., material topics identified through the DMA, strategic targets and contribution to the SDGs.

Connectivity matrix12

| Strategic pillars and guiding principles | Stakeholder | Material topic | Strategic targets | Progress 2025 | SDGs |

|---|---|---|---|---|---|

| Financial self-reliance and inclusion |  | Equal treatment and opportunities for all | Gender diversity | 34% female in Top management |   |

| Consumers and end-users | Impact investing NPS-i | 10.1% 25.0 |   | |

| Affected communities | - | - |  | |

| Vitality and sustainable employability | | Own workforce | Employee engagement | 773 | |

| Workers in the value chain | - | - | - | |

| Sustainable living and climate | | Climate change | Carbon footprint reduction | 8.6% | - |

| Impact investing | 10.1% |   | |||

| Biodiversity and ecosystems | Carbon footprint reduction | 8.6% |  | |

| Impact investing | 10.1% | | |||

| Resource use and circular economy | - | - | | |

| Upholding standards | | Business conduct and corporate culture | - | - | |

| Value over volume, cost-efficient and financially robust |  | - | Solvency II ratio | 218% | - |

| Organic capital creation | € 1,315 million | ||||

| Operating return on equity | 14.1% | ||||

| Dividend per share | € 3.41 | ||||

| Share buyback | € 230 million | ||||

| Combined ratio (P&C and Disability) | 92.2% | ||||

| Revenue growth (P&C and Disability) | 3.0% | ||||

| Pension buy-outs | € 2,810 million | ||||

| Pension DC inflow | € 3,011 million | ||||

| Annuities | € 646 million | ||||

| Fee-based business operating result | € 186 million |

- This connectivity matrix serves as overview of how a.s.r.'s strategy, stakeholder groups and material topics are connected. Please note that other connections that are not shown in this matrix may exist as well.

- Please note that the strategic target Sustainable reputation is an overarching target that cannot be linked directly to one or more material topics, and is rather an outcome of the efforts on all its material topics. For more information about this strategic target, see sections 2.4.1.2 and 6.5.

- Based on the most recent pulse check assessment from January 2026. The annual extensive culture scan, conducted in February 2025 had 71 as a result.

- Section 2.4.2 is in scope of CSRD and limited assurance (ESRS 2 SBM-1).

2.5 Trends and developments

Global and regional trends and developments continue to influence the environment in which a.s.r. operates. a.s.r. aims to adapt to these evolving circumstances and remains proactive in addressing risks and opportunities associated with these changes. Sections 5.4 and 7.8 provide further detail on the risk management approach, which forms an integral part of a.s.r.’s day-to-day operations. The trends and developments discussed in this section highlight the market dynamics most relevant to a.s.r., their impact on stakeholders and the organisation's response to these changes.

2.5.1 Political, financial and legislative

a.s.r. has identified three pivotal trends shaping the industry in the current political and financial market landscape:

Increased geopolitical uncertainty due to conflicts in several areas in the world, and recent election results affect international stability and increase trade tensions.

Economic pressure from wage increases, inflation, rising housing prices, and increasing labour shortages is significant.

Impact of legislative developments, such as the Future Pensions Act (Wet toekomst pensioenen - Wtp), sustainability regulations, Solvency II review and the European Artificial Intelligence (AI) Act.

Impact on a.s.r. and its stakeholders

Persistent inflation, volatile interest rates and geopolitical uncertainty have led to tempered growth projections of around 3% for the global economy. Although a decline in inflation is expected, it remains moderate to high, especially in the Netherlands. Uncertainty persists due to volatile interest rates and recession fears. Customers face uncertainty regarding resources, security and purchasing power, but this also might raise concerns about the stability and profitability of a.s.r.

Changes in the regulatory and supervisory environment could lead to stricter oversight and more frequent investigations, whilst many new regulations need to be interpreted and implemented within a short period of time, though not all regulations are final yet. The evolving regulatory landscape leads to increased internal costs and demands swift implementation of new rules. In the near term, the Wtp reshapes the Dutch pension market. Smaller insurers and intermediaries may struggle to comply with these developments, potentially leading to market consolidation and growth opportunities for a.s.r. Political pressure, especially from US stakeholders, challenges sustainability and diversity commitments.

a.s.r.'s response

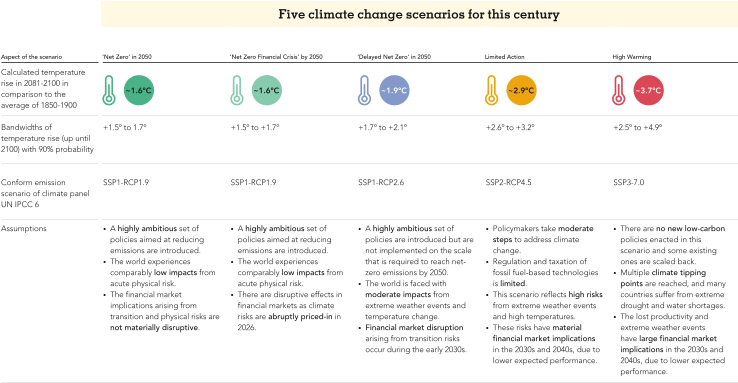

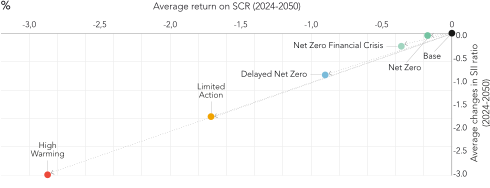

a.s.r. assesses geopolitical developments and explores various potential economic scenarios. Financial planning includes scenario analysis and stress testing to ensure resilience under various macroeconomic conditions, while maintaining a cautious yet forward-looking approach in its capital allocation. a.s.r. aims to further diversify its investment portfolio; for more information, see section 7.8. In response to heightened protectionist policies, a.s.r. reviews operational dependencies and supplier risk exposure. Additionally, a.s.r. may adjust premiums, while remaining an affordable insurer for its consumers.

As pension funds reassess their strategic options under the new legislation, a.s.r. is well‑positioned to support them with de‑risking solutions such as full and partial buy‑outs, leveraging its expertise and ability to offer long‑term security for participants.

a.s.r. monitors and assesses relevant legislative and regulatory developments and implements appropriate control measures. To manage regulatory changes, a.s.r. initiates programmes for their implementation (e.g. CSRD, DORA, European AI Act). a.s.r. remains committed to ESG goals despite international developments, whilst closely monitoring the international regulatory climate to ensure alignment and credibility. For more details, see section 6.

2.5.2 Technological

The following three technological trends have the greatest impact on a.s.r.'s operating environment.

Digitalisation and big data continue to drive regulatory changes to balance innovation, customer protection and financial stability.

AI promises to deliver speed and simplicity in business processes and insurers are experimenting and implementing cost-efficient technologies at a faster pace, with the potential of gaining an competitive advantage.

Cyber security and cyber threats remain persistently high, which has resulted in new or renewed cyber and information security requirements, as well as data-focused legislation, including the DORA and the European AI Act.

Impact on a.s.r. and its stakeholders

Technological innovations are key for competitiveness and enable better services and efficiency, enhancing customer experience for clients for a.s.r. Generative AI and artificial general intelligence are reshaping services and risk modelling in the insurance industry. Insurers are developing and implementing cost-saving technologies in areas such as claims management, underwriting, risk prediction and customer contact moments. However, greater cloud presence and data sharing increase cyber risks, such as data leaks, hacks and social engineering. The increased risk of cyber attacks make financial institutions more vulnerable to cyberattacks1. Financial institutions are expected to accelerate automation and decision-making, while also raising new ethical, regulatory and operational considerations for insurers like a.s.r.

For customers, technological innovation leads to easier access to products and better customer service on the one hand, and to increased risk of cybercrime on the other2. Customers might also feel overwhelmed or dissatisfied with the shift towards digital services, which in turn might impact the customer experience.

The Dutch Central Bank (De Nederlandsche Bank - DNB) has warned the financial sector about increased cyber risk linked to geopolitical instability3, potentially leading to data breaches, financial losses and damage to reputation. In 2025, these global dynamics continued to evolve.

a.s.r.'s response

a.s.r. actively adopts AI and technological developments for automation and customer interaction, taking ethical, regulatory, security and sustainability considerations into account. Its customer contact strategy incorporates the requirements of the new European Accessibility Act and ensures consistent service, supported by tools such as chatbots that help claim handlers locate relevant policy provisions and generate draft responses to questions from customers. Another example is the digitalisation strategy of a.s.r. health, which has made significant progress in both digitalisation and the application of AI. For further details, see section 4.2.4. This strategy provides a strong foundation for broader application across a.s.r.

Cyber resilience is priority for a.s.r. It implements internal and supplier controls, collaborates with National Cyber Security Centre (NCSC) and the Digital Trust Centre (DTC), and invests in prevention, detection and response technologies. Awareness is being raised through gamification and phishing campaigns. For details, see section 5.4.3.

- Source: BCG (2024)

- Source: DNB (2024)

- Source: DNB (2024)

2.5.3 Environmental and social

a.s.r. outlines three key environmental and social trends that impact the company and its stakeholders.

The ever-increasing importance of climate change, resource scarcity and loss of biodiversity, and risks related to insurance coverage gaps.

In the Netherlands, the declining population growth rate and ageing population are putting pressure on the labour market and have led to reforms of pension and self-employment legislation, such as the Employment Relationships Deregulation Act (Wet Deregulering Beoordeling Arbeidsrelaties - DBA).

Impact on a.s.r. and its stakeholders

Environmental risks affect insurability and investment strategies. Physical risks (e.g. extreme weather) and transition risks (e.g. regulation changes and technological developments) challenge traditional insurance models, raising critical questions about insurability and risk-sharing mechanisms. This can lead to higher claims and increased insurance costs, and as a result policyholders might face higher premiums. Additionally, environmental risks potentially affect the value of a.s.r.'s investment portfolio.

The labour market remains tight due to an ageing workforce, alongside a growing demand for new skills, resulting from the technological developments described in section 2.5.2. Although partly offset due to the new DBA, the rise in self-employment and freelancing is affecting labour market dynamics, employment ratio and the demand for pension and disability products. The DBA is also raising uncertainties on income security and is having an impact on how self-employed workers look at pension and disability products.

a.s.r.'s response

a.s.r. aims to minimise its climate impact and contribute to climate change mitigation and adaptation. a.s.r. integrates considerations of climate change, resource scarcity and biodiversity loss into its investments, products and services. To manage transition risks, a.s.r. collaborates with knowledge partners to learn about and apply technological insights in risk management, client acceptance and pricing. For details, see section 7.8.1.2.

Intensifying climate events challenge insurability and risk-sharing. a.s.r. responds by innovating product design and pricing, and investing in data-driven risk modelling. Scenario analysis and stress testing are used to assess portfolio resilience under various climate pathways. On the other hand, a.s.r. engages in public discussions about the insurance protection gap that arises as a result of the increased environmental and social risks.

a.s.r. seeks the best solution for every capacity requirement through total workforce management. Solutions vary between hiring new and permanent employees or flex workers, or internal staff movements resulting from the Aegon NL integration or talent planning.

Interview: Ingrid de Swart on Artificial Intelligence

Interview: Ingrid de Swart on Artificial Intelligence

Artificial Intelligence: from

exploration to acceleration

COO/CTO Ingrid de Swart describes 2025 as 'a pivotal year' when asked about Artificial Intelligence (AI). In January, the Management Board (MB) and Board of Directors attended an intensive AI programme at INSEAD. ‘For three days, we immersed ourselves in this technological development. Inspired by its opportunities, we concluded that this is something worth pursuing.’

In the months that followed, large groups of employees received training, INSEAD professors gave lectures, and colleagues developed practical AI use cases. These range from customer service and employee self-service to applications at the core of the organisation, such as the Smart Claims Assistant (SCA). ‘This in-house developed tool enables personal injury claims handlers to locate information faster in complex files through a smart summary with references. Integrating technology into the claims process affects one of the insurer's key activities. The SCA is fast and delivers high-quality output. Because personal injury claims handlers are scarce, the solution helps maintain quality and timeliness. Employees using it are very enthusiastic.’ To stimulate further development, the MB asked itself in Q3 2025: how can the use of AI be accelerated?

And what was the answer?

‘Technology alone is not enough. The existing organisation must adapt. This requires changes in working practices, new skills and close collaboration between business and technology.’

That sounds like considerable changes lie ahead for employees.

‘That is correct, which is why employee involvement is essential. Through an extensive AI development programme, employees learn how AI can help them in their work. I strongly believe that our work will change for the better. With the SCA, for example, time spent on repeatedly familiarising themselves with files is reduced, creating more time for substantive tasks. This makes work more engaging. At the same time, it is important that AI does not make work monotonous, which is why tasks are combined thoughtfully. Strategic workforce planning shows that, through natural attrition and talent development, there is sufficient capacity to absorb change. This approach ensures employees grow alongside these developments.’

What opportunities do you see for applying AI in services to customers and advisers?

‘The SCA shortens processing times for customers. A similar solution exists in Health, where a knowledge management system functions as an intelligent Q&A. Employees can ask questions about specific types of cover, and the system provides accurate information quickly. This ensures consistent, high-quality responses to customers. Our measurements show that customer satisfaction in Health is increasing faster than elsewhere in the organisation. Such systems can also support advisers by enabling quick responses to their questions, allowing them to focus on customer contact. Ultimately, this contributes to higher customer satisfaction and stronger cooperation with intermediaries.’

How does a.s.r. guarantee personal attention for customers in a digital world?

‘Tasks such as address changes, what we call low-impact contact, should be fast and simple. However, customers dealing with high-impact situations, such as damage after an accident or a mortgage application, need a human approach. Automating straightforward processes with AI frees up time for employees to support customers who need expertise and empathy. AI also help us add value for customers by enabling more personalised engagement, for example by approaching customers based on specific characteristics, such as age.’

In what way can AI improve a.s.r.’s sales channels?

‘Since our training at INSEAD, efforts have accelerated. With the establishment of a new Online Unit, direct and digital sales have become a strong focus. Customers, particularly younger ones, expect convenience and speed. We are therefore investing in a fully online experience, improving the customer journey through enhanced online propositions, streamlined sales funnels and strengthened digital customer service. Work is carried out in multidisciplinary teams, with collaboration across product lines central to accelerating the strategy with AI.’

Can you elaborate?

‘Initially, each business unit had its own approach to AI. Understandable, but it limited opportunities to learn from each other and to benefit from economies of scale. Returning to the SCA: if it works for P&C, why not explore similar solutions for Disability or Mortgages? The same applies to pricing. Dynamic pricing is used in Pensions, and now AI enables customised pricing in Disability. Sharing knowledge and working together accelerates progress and avoids duplication. AI also strengthens collaboration between business units and IT. Success lies in multidisciplinary teams that experiment, provide feedback and continuously improve models. This enables the organisation to maximise the potential of technology - controlled, yet with courage to innovate.’

Innovation costs money. Is AI already delivering a return on investment?

‘At use-case level, the benefits are already visible. Faster and more efficient processes reduce costs and increase employee and customer satisfaction. The SCA also helps reduce claims costs. I am convinced that AI can accelerate a.s.r.’s strategy, facilitate growth and further strengthen competitiveness. Investments in cloud solutions and data infrastructure make AI deployable across the organisation. This requires time and resources, but the potential impact is substantial.

At the same time, AI brings challenges, including energy use and broader implications for people and processes. That is why a.s.r. makes conscious choices guided by ethical principles, human oversight and sustainability ambitions. By optimising processes and increasing scalability, AI helps reduce operational costs and contributes directly to long-term value creation for our stakeholders. I expect 2026 to be an important year in which this impact becomes truly visible. AI will also be addressed during a.s.r.’s Capital Markets Day in 2026, where the organisation will share its developments on this topic.’

This page is intentionally left blank.

3 How a.s.r.

operates

3.1

Becoming the best financial service provider

Complaints management(score between 0-10)8.1 2024: 8.4 | Complaints fully handled(in %)70 2024: 74 | Engagement by topic |

Impact investments(in % of total AuM)10.1 2024: 8.7 | NPS-i(-100 to 100)25.0 2024: 18.41 | |

Green lease contracts(as % of total new contracts)100 2024: 99 | Increase of average energy label(in energy label steps)1.8 2024: 1.6 | |

| 1 Please note that the 2024 figure represents the Q4 baseline value. |

a.s.r. aims to create long‑term value for its key stakeholders: customers, employees, shareholders and society. a.s.r. strives to be the best financial service provider for its customers and intermediaries. It offers simple and transparent products and services that meet customers’ needs, including sustainable solutions. To become the best in the industry, a.s.r. embraces technological developments and applies them where they add value. a.s.r. is data‑driven and incorporates customer feedback into its decision‑making. By leveraging technological innovations, including Artificial Intelligence (AI), a.s.r. continuously improves its services. Society can expect a.s.r. to integrate social and environmental objectives into its strategy.

3.1.1 Business conduct

3.1.1.1 Customer focus

Customer research

Beyond price and product quality, consumers are increasingly aware of social and environmental challenges such as climate change and inequality. These concerns influence their purchasing behaviour, including their choice of financial service providers. To remain aligned with customer expectations, a.s.r. conducts ongoing research into consumer attitudes, focusing on topics such as sustainability, inclusivity and responsible business practices. This provides valuable insights that help guide product development.

NPS-i

To measure customer loyalty and improve service quality, and to gain insight into customer interactions across all channels, a.s.r. measures the interaction Net Promoter Score (NPS‑i). This unified metric combines offline interactions (NPS‑c) and digital interactions (NPS‑d) into a single consolidated score, enabling real‑time insights at key moments in the customer journey. This approach supports the continuous improvement of both digital and employee‑assisted interactions with customers.

The growth ambition for NPS‑i over the next two years is an increase of 4 points, from a baseline of 18.41 to 22.4 by the end of 2026.

NPS-i2

Key developments in 2025

In 2025, a.s.r. made further progress in strengthening customer centricity and improving the customer experience across online and offline channels. The NPS‑i increased from 18.4 in 2024 to 25.0 in 2025, with and NPS-d score of 6.4 and the NPS-c score of 53.6.

The NPS‑c remained consistently high during 2025. The completion of major migrations, including those for Individual life & Funeral, Pensions and Mortgages, resulted in enhanced data consistency and improved support for customer processes. These developments are a prerequisite for reliable and personalised customer service.

The NPS-d continued to improve in 2025, supported by targeted optimisations in customer journeys and the implementation of several content-related quick wins. Digital self-service usage was further strengthened by AI-enabled applications. These developments contributed to improved navigation, higher levels of self-service and greater consistency across digital touchpoints.

For the results specified by business line, see section 9.2.4.

Strengthening the digital customer experience

The target for the NPS‑i has been achieved. As more processes become digital, the NPS‑d will have an increasing significant influence on the overall NPS‑i score. Therefore, a.s.r. focuses on further improving the digital experience, completing the remaining migrations and safeguarding data quality remains essential in 2026 to realise the stated ambitions.

In 2026, the emphasis will be on improving the NPS‑d. a.s.r. aims to expand the use of AI as an accelerator to enhance the customer experience, making processes smarter, more efficient and more scalable by increasing self‑service options and enabling straight‑through processing.

Raad van Doen: Involving customers and advisors

The Raad van Doen is an online panel where customers, advisers and entrepreneurs actively contribute to shaping a.s.r.’s products, services and communications. The panel includes approximately 8,000 participants who regularly take part in short surveys, tests and co-creation sessions. Their feedback provides valuable insights that directly supports improvements in customer journeys, product development and sustainability initiatives, ensuring that decisions truly reflect customer needs.

In 2025, a.s.r. expanded the Raad van Doen with an Entrepreneurs Panel to better align with the needs of self‑employed professionals, SMEs and employers. Their contributions help ensure that a.s.r. delivers relevant, user‑friendly and future‑proof solutions for all customer groups.

The Digital Programme

As customer engagement methods and business processes become increasingly digitalised, a.s.r. aims to deliver effective customer interactions and operational efficiency. This approach seeks to reduce costs through AI-driven process efficiency, improve customer experience (NPS-i), and drive growth through direct and intermediary channels.

This ambition is built on three main pillars:

Standardising customer communication channels: Unified service touchpoints create a consistent customer experience across business lines.

Reducing low-impact interactions: Smart self-service and proactive communication help to avoid unnecessary contact.

Providing optimal high-impact interactions: Personal, empathetic service for complex customer situations where human interaction is valued by the customer.

Key developments in 2025

In 2025, a.s.r. implemented and expanded several core digital enablers to support data-driven and customer-centric operations. Key initiatives included the development of Master Data Management to ensure consistent data quality across systems, and the enhancement of Customer Relationship Management (CRM) through a cloud-based omni-channel contact centre and CRM platform. Additionally, a Top Task Dashboard was developed to optimise key customer journeys. To enable innovation and support the AI roadmap, a.s.r. increasingly leverages the public cloud. In 2025, a.s.r. embarked on an ambitious multi-year journey to migrate all workloads to the public cloud. This transition will facilitate innovation, improve efficiency and enhance IT security.

During the integration of Aegon NL, special attention is given to digital customers through the ‘Warm Welcome’ programme, designed to retain them as users of a.s.r.'s services. In recognition of these efforts, a.s.r.’s customer website was rated most popular in the Insurers category of the Website of the Year (Website van het Jaar) 2025 awards. This external acknowledgement reflects the ease of use and the trust customers place in a.s.r.’s digital channels, underscoring the success of a.s.r.’s digitalisation strategy and its ambition to provide exceptionally intuitive and personal services.

Finally, to enhance readability, a.s.r. has aligned its consumer website with Dutch B1 language level.

- Please note the 2024 figure represents the Q4 baseline value.

- Please note the 2024 figure represents the Q4 baseline value.

3.1.1.2 Prevention of payment problems

a.s.r. makes considerable efforts to ensure that its customers are financially self-reliant and aims to minimise the number of policy cancellations caused by payment arrears and related issues. The organisation takes proactive measures to prevent situations where customers incur additional costs and it strives to avoid payment defaults.

a.s.r.'s memberships and coalitions enable cross-sector knowledge sharing, helping to improve customer processes and services related to payment problems.